Learning from mistakes

I decided to do two insight posts this month as I have missed a couple of the past months."Mistakes are the portals of discovery"~ James Joyce

In statistics there is a test for hypothesis which looks at the hypothesis prediction and the actual outcomes over many experiences. The less errors the more robust the hypothesis.

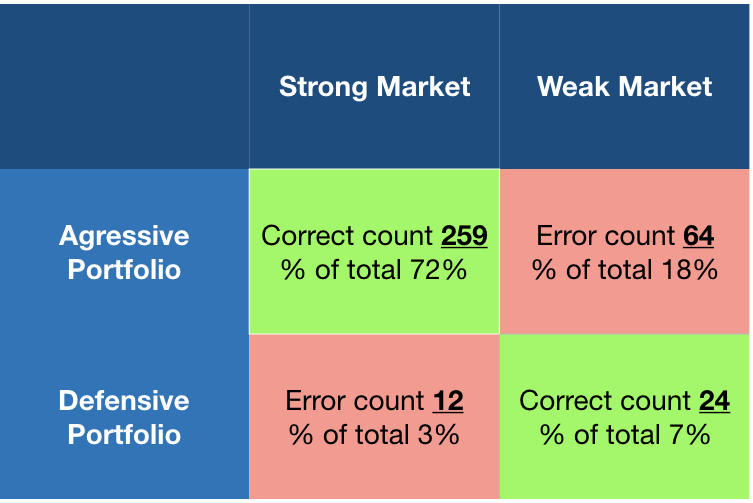

I decided to do this for my model going back as far as I could. I was curious about my ability to protect in down markets and yet still take advantage of up markets. For my review I called any year where fixed income did the best as a down market and all other years up markets. In alignment with this I looked at my calls and if I had called for a fixed income investment then that was a defensive portfolio, all others were aggressive portfolios. The results are:

Total periods: 359

Analysis: These results show what I expected. I am capturing 96% of the strong markets (259 of the 271 strong market periods) while still avoiding 27% of the weak market periods (24 of 88). This has allowed the portfolio to accumulate almost all of the strong market results while still dampening over a quarter of the negative periods.

This is what I would hope for, that is if I have to have errors I want more of them to be with an aggressive portfolio as I am trying to capture all the upside while avoiding as much downside as possible. Overall I have been right almost 80% of the time, (283 of 359) based on this metric.

There is no guarantee going forward, but so far so good.

Comments

Post a Comment